As the total amount

of funds invested through ICOs in blockchain-related ventures reaches twelve

billion dollars (Q1-2018) accounting for more funds raised than the entire 2017

[1], it becomes paramount to gain a crisp understanding of which business models

may be leveraged to deliver on the promises to build a new breed of solutions

harnessing the potential of the internet of value.

With this awareness

in mind, we (Michele Osella, Riccardo Rostagno and myself) set off to

conduct an international exploratory study on the business models emerging in

the ecosystem of public blockchains. More specifically, the study aimed at

answering the following research questions:

RQ #1: Along which

dimensions can the blockchain ecosystem be mapped?

RQ #2: What are the

key archetypal actors and their strategic positioning?

RQ #3: What

emerging business models are enabled by blockchain?

To answer the above

questions, thirty-two ventures leveraging public blockchains were analysed,

resulting into twenty business models identified. In the remainder of the post,

I will briefly outline the highlights of the study while a more comprehensive

view of the results obtained may be found in the presentation linked at the

bottom of the post.

A number of notable

attempts have been made so far to map the blockchain ecosystems (eg: Lange and Nussbaum, to name a few). Nevertheless,

despite being commendable efforts, most of the early outputs generated suffered

from a number of methodological shortcomings having to do with lack of

exhaustivity as well as lack of homogeneity in the categories used. We are thus

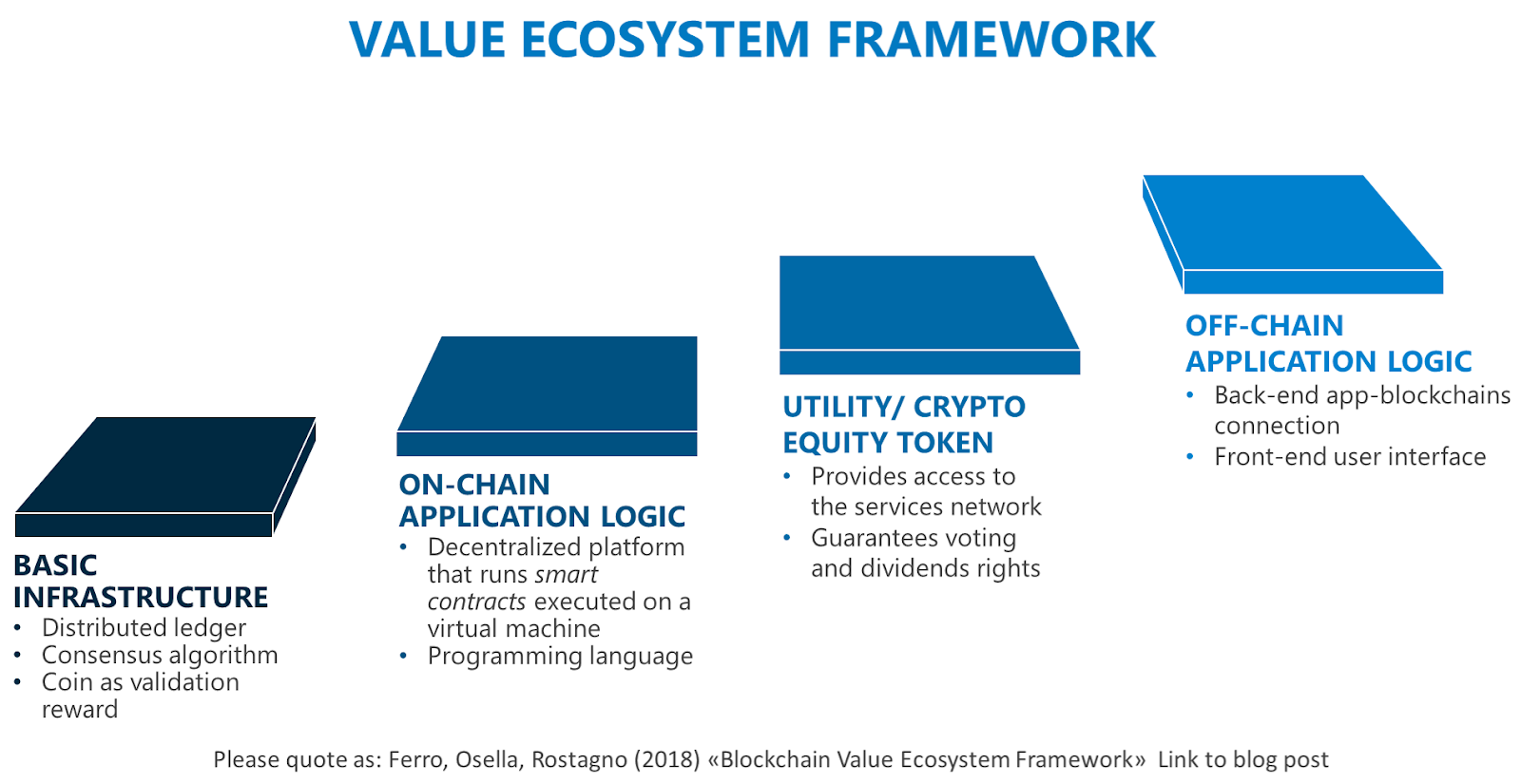

proposing a “blockchain value ecosystem framework” (see Figure 1) as a first

step toward overcoming the issues listed above. The framework identifies four

technological layers clarifying the primary ingredients constituting a

blockchain-based solution. It consists of a simple yet clear representation

that may help companies in understanding what DLT (distributed ledger

technologies) may offer and how to approach them.

Figure 1. Blockchain value

ecosystem framework

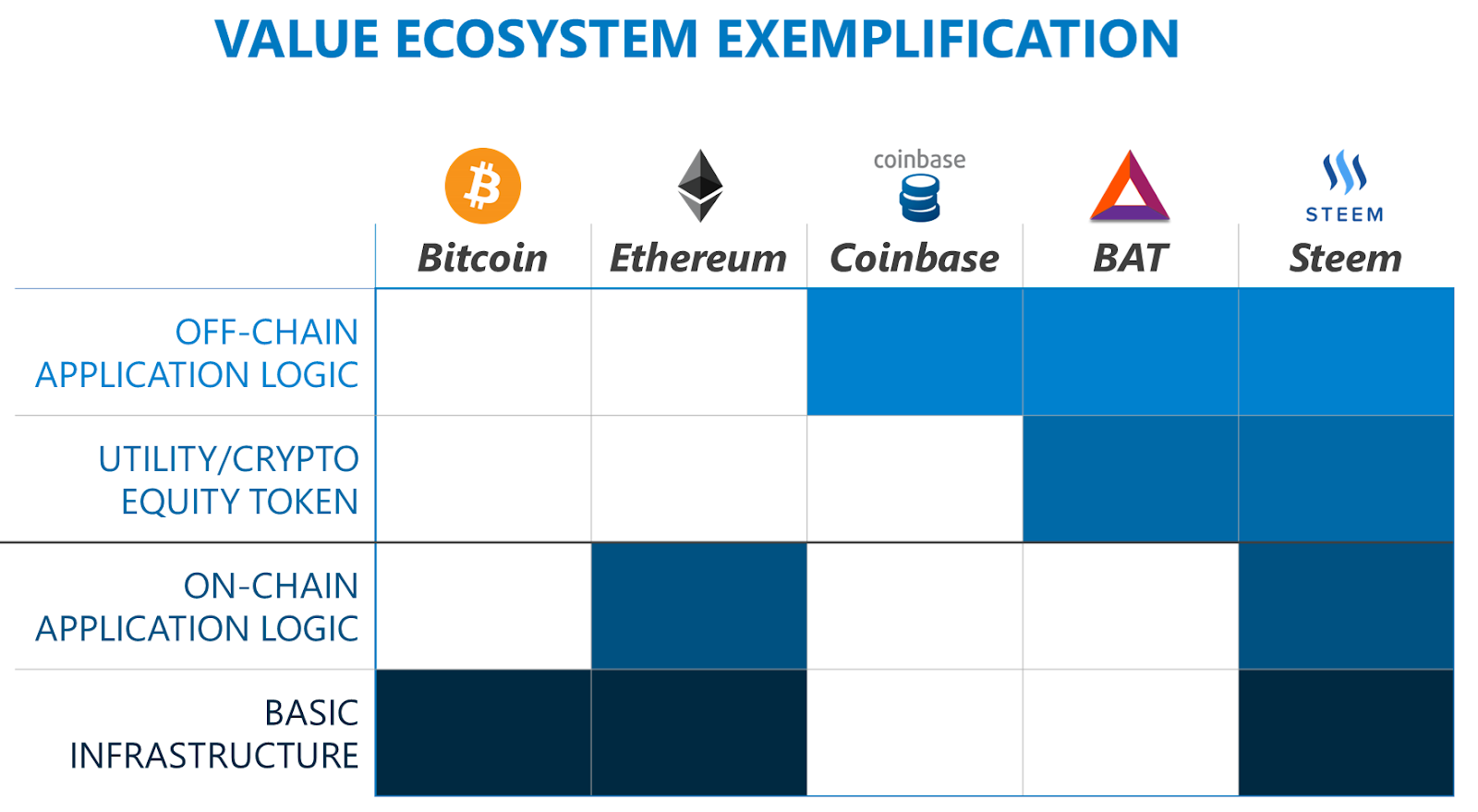

In the picture below (Figure 2), a few real life actors have been mapped against the framework to

exemplify how it may be used to understand the different levels of vertical

integration that any given company may decide to adopt with respect to

blockchain absorption. It goes without saying that the higher the level of

integration the higher the requirements in terms of technological skills and

financial resources necessary for developing and adopting a blockchain-based

solution.

Figure 2. Map of real life actors

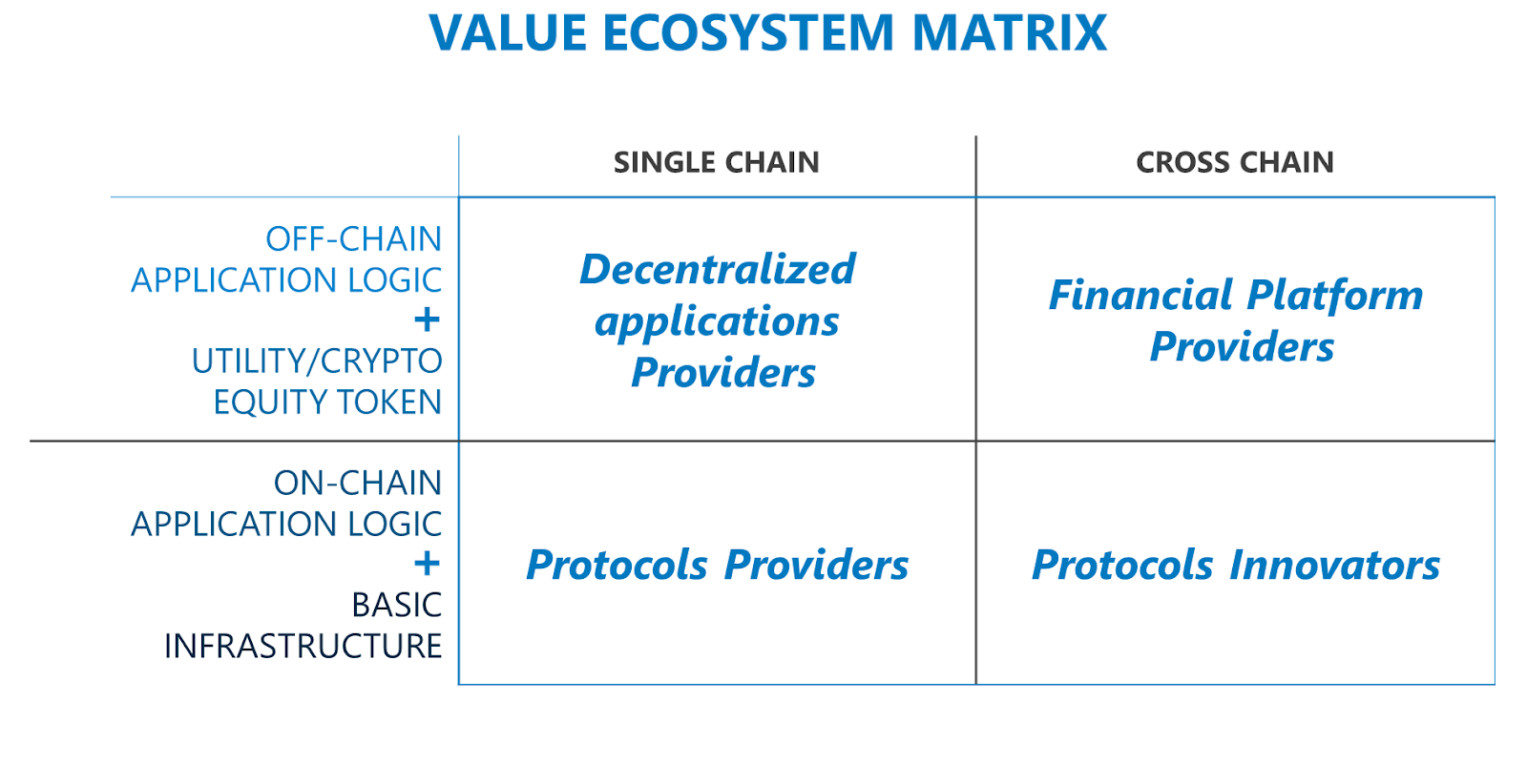

For the

classification of the key archetypal actors and their strategic positioning

with respect to the different blockchains available on the market, the

framework was complemented with an additional dimension considering whether the

company analysed was operating on a single blockchain or on multiple

blockchains. This resulted in a two by two ecosystem matrix answering RQ #1 and

identifying four strategic positions, one for each quadrant (Figure 3):

- Decentralized-application Providers

- Protocol Providers

- Financial Platform Providers

- Protocol Innovators.

Figure 3. Four strategic

positions

By placing the

ventures analysed in the different quadrants, it was subsequently possible to

cluster them into eleven archetypal actors (RQ #2): five of which positioned in

the distributed-applications providers quadrant and two situated in each of the

other quadrants (Figure 4). In this respect, it is important to note that while

DLTs are still in an “infrastructural phase”, that is to say a phase in which

enabling infrastructures are still being developed, a dominant design has not

emerged yet and most of the value generated is captured by the lower layers of

the technological stack [2]. Moreover, the upper left quadrant - where

distributed applications (DApp) are designed - represents a very fruitful

business model innovation sandbox for devising approaches that have the

potential to disrupt large rent-seeking incumbents across many different

industries in the long-term.

Figure 4. Eleven archetypal

actors

From the analysis

of the real life actors, it was subsequently possible to single out one or more

business models that could be associated to each archetypal actor. To

exemplify, among the mining companies analysed, four business models were

identified: (1) solo mining in which

the mining activity is conducted by a single company fully shouldering the

infrastructural costs and the risks associated with the mining activity; (2) pool mining in which companies are

sharing their infrastructure and the risk associated to mining; (3) cloud mining in which the company is

renting its computing infrastructure to third parties thus shifting the risk

associated with mining on the clients; and (4) mining marketplaces that are acting as brokers between

infrastructure owners and buyers of mining services.

Due to length

constraints, it is not possible to discuss in-depth all the business models

identified, nevertheless for each of them a Business Model Canvas explaining

the underlying value logic has been inserted in the appendix of the

presentation linked at the bottom of the post.

Figure 5. Twenty emerging business models

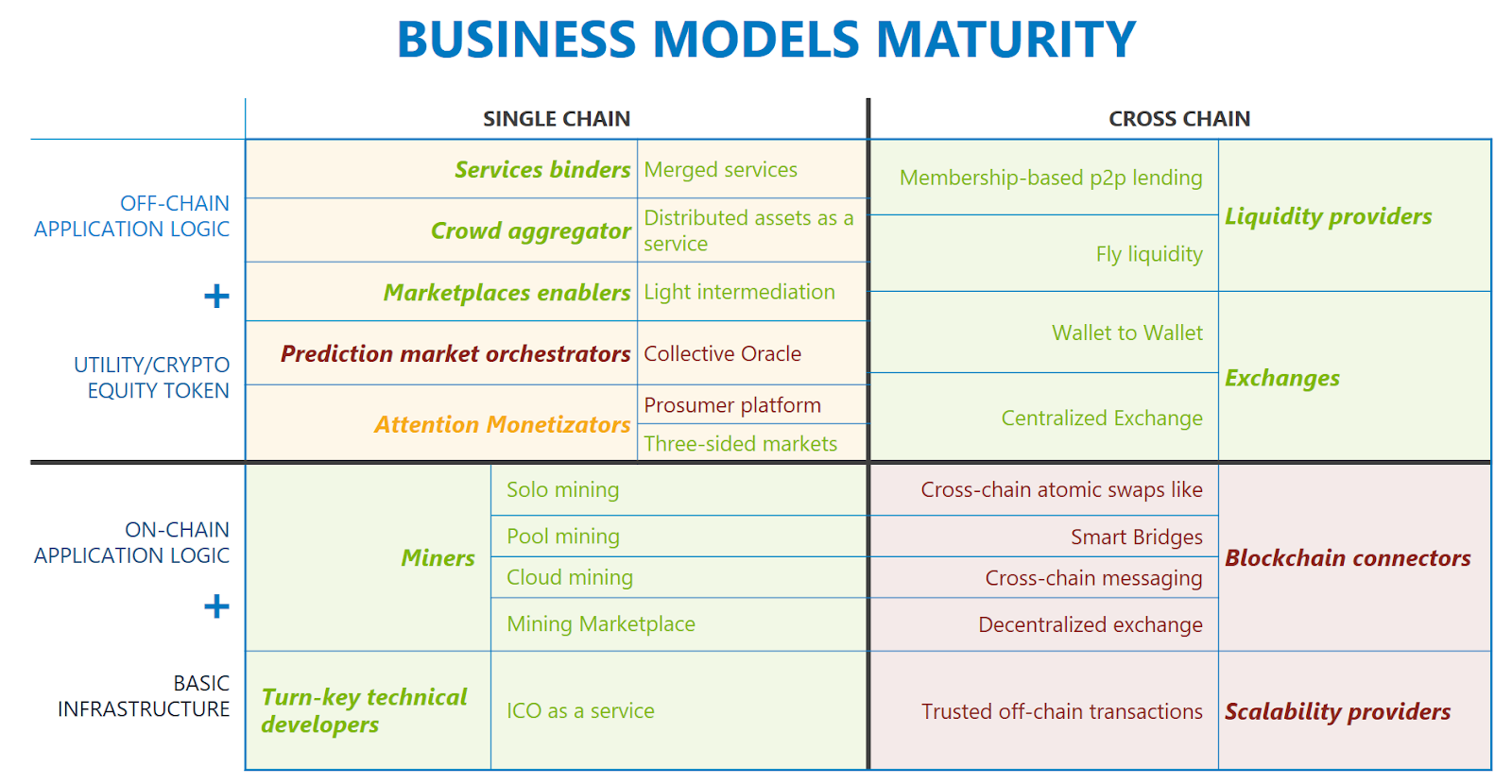

Finally, the

analysis of the thirty-two ventures brings to the fore dissimilar maturity

levels in terms of business model robustness for the various quadrants. More

specifically, the quadrants of protocol providers (lower-left) and that of

financial platform providers (upper-right) show a higher level of maturity in

terms of presence of a wide users’ base, identification of a clear value

proposition and tested value appropriation mechanisms. For what concerns the

other two quadrants instead, the situation is diversified among the actors

operating in the distributed applications quadrants (upper-left) while a low

level of maturity is present in the protocol innovators quadrant (lower-right)

which is made up of companies that are still exploring possible business models

for solving technical scalability issues.

Figure 6.

Business models maturity

To conclude this

post, we would like to share a number of reflections on the relationship

between blockchain and business strategy spurred by the analyses conducted

during the exploratory study.

First, a clear

understanding of the ingredients composing a full stack blockchain-based

solution needs to be acquired by CEOs willing to leverage blockchain in their

core business activity. In this respect, the blockchain value ecosystem

framework provides an accurate yet intuitive instrument for choosing the

appropriate level of vertical integration in the adoption and development of

blockchain-based solutions.

Second, four

strategic positions were identified with significant differences in terms of

capital intensity, technical proficiency required and depth of understanding of

the overall blockchain ecosystem. Choosing the right position for a venture

requires a careful analysis of the presence, possibility to access and ability

to manage the above aspects.

Third, twenty

business models were mapped with different levels of maturity with respects to

their ability to clearly identify their value proposition and the mechanisms

for capturing part of the value created. In this respect, the availability of

significant financial resources for startups at a very early stage of development combined with the presence of

seigniorage economic benefits coming from the possibility to mint tokens, in

many instances has reduced the pressure on cash flows thus allowing companies

to focus more on technical challenges. While this in the short-term this may

help raising the level of technological excellence of the blockchain ecosystem,

in the long-run it could pose serious sustainability challenges.

Finally, from a business model perspective, the emergence of blockchain technologies seems to

have generated three types of innovations: (1) the birth of business models for

blockchain-specific activities such as mining; (2) the possibility to combine

into a single business model activities previously conducted by different

players (eg: payments & reputation, chat & payments); (3) the emergence

of light intermediation opportunities in which the middleman may adopt

revenue-sharing mechanisms that promote a fairer redistributions of the overall

value generated by all the engaged stakeholders.

Should you be

interested in discussing more in depth the results of the study, don’t hesitate

to get hold of me via Linkedin or Twitter.

Research wants to be free, but it is costly to produce. Please consider supporting our market education activity by making a donation.

EOS account: cryptoenrico

BTC: https://tippin.me/@egferro

Enrico Ferro.

[1] Coindesk, 2018, “State of Blockchain Q1

2018” Retrievable at link

[2] Pantera

Capital, 2017, “VC’s Missing 97% of the Trade” Retrievable at link

Business Models for Blockchain-based Ventures from Enrico Ferro

Watch my interview with David Orban in which we talk about business models for blockchain.