As the total amount

of funds invested through ICOs in blockchain-related ventures reaches twelve

billion dollars (Q1-2018) accounting for more funds raised than the entire 2017

[1], it becomes paramount to gain a crisp understanding of which business models

may be leveraged to deliver on the promises to build a new breed of solutions

harnessing the potential of the internet of value.

With this awareness

in mind, we (Michele Osella, Riccardo Rostagno and myself) set off to

conduct an international exploratory study on the business models emerging in

the ecosystem of public blockchains. More specifically, the study aimed at

answering the following research questions:

RQ #1: Along which

dimensions can the blockchain ecosystem be mapped?

RQ #2: What are the

key archetypal actors and their strategic positioning?

RQ #3: What

emerging business models are enabled by blockchain?

To answer the above

questions, thirty-two ventures leveraging public blockchains were analysed,

resulting into twenty business models identified. In the remainder of the post,

I will briefly outline the highlights of the study while a more comprehensive

view of the results obtained may be found in the presentation linked at the

bottom of the post.

A number of notable

attempts have been made so far to map the blockchain ecosystems (eg: Lange and Nussbaum, to name a few). Nevertheless,

despite being commendable efforts, most of the early outputs generated suffered

from a number of methodological shortcomings having to do with lack of

exhaustivity as well as lack of homogeneity in the categories used. We are thus

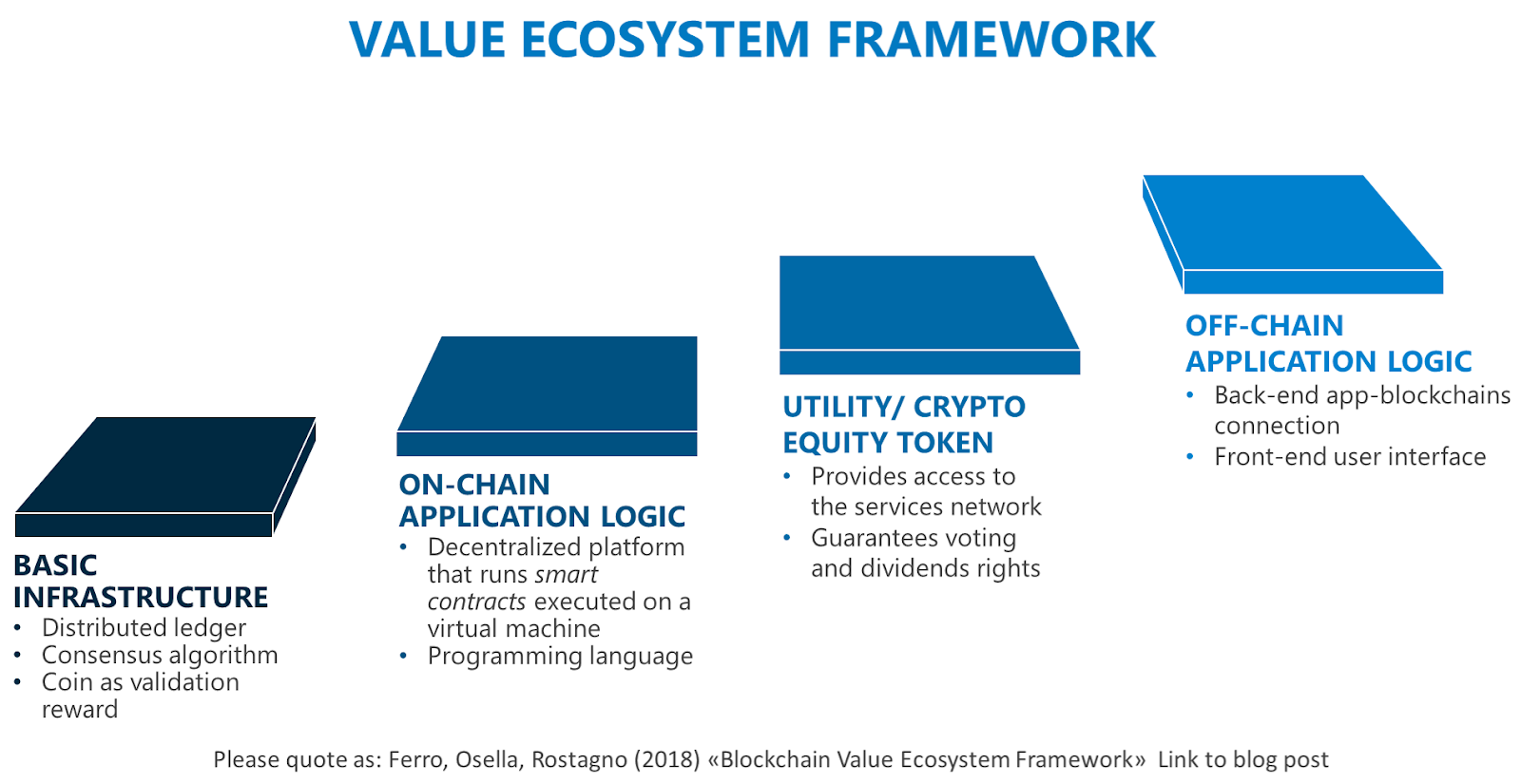

proposing a “blockchain value ecosystem framework” (see Figure 1) as a first

step toward overcoming the issues listed above. The framework identifies four

technological layers clarifying the primary ingredients constituting a

blockchain-based solution. It consists of a simple yet clear representation

that may help companies in understanding what DLT (distributed ledger

technologies) may offer and how to approach them.

Figure 1. Blockchain value

ecosystem framework

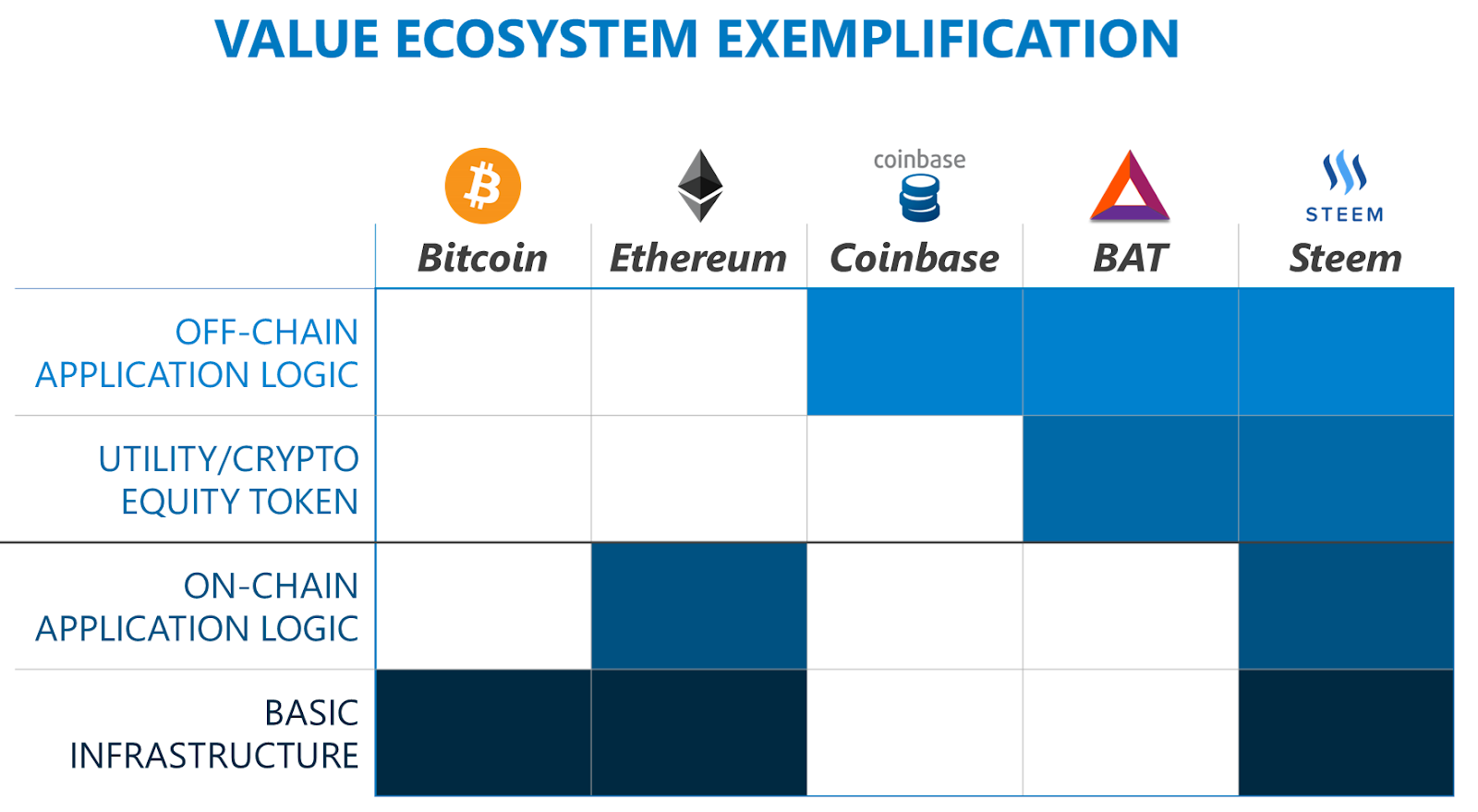

In the picture below (Figure 2), a few real life actors have been mapped against the framework to

exemplify how it may be used to understand the different levels of vertical

integration that any given company may decide to adopt with respect to

blockchain absorption. It goes without saying that the higher the level of

integration the higher the requirements in terms of technological skills and

financial resources necessary for developing and adopting a blockchain-based

solution.

Figure 2. Map of real life actors

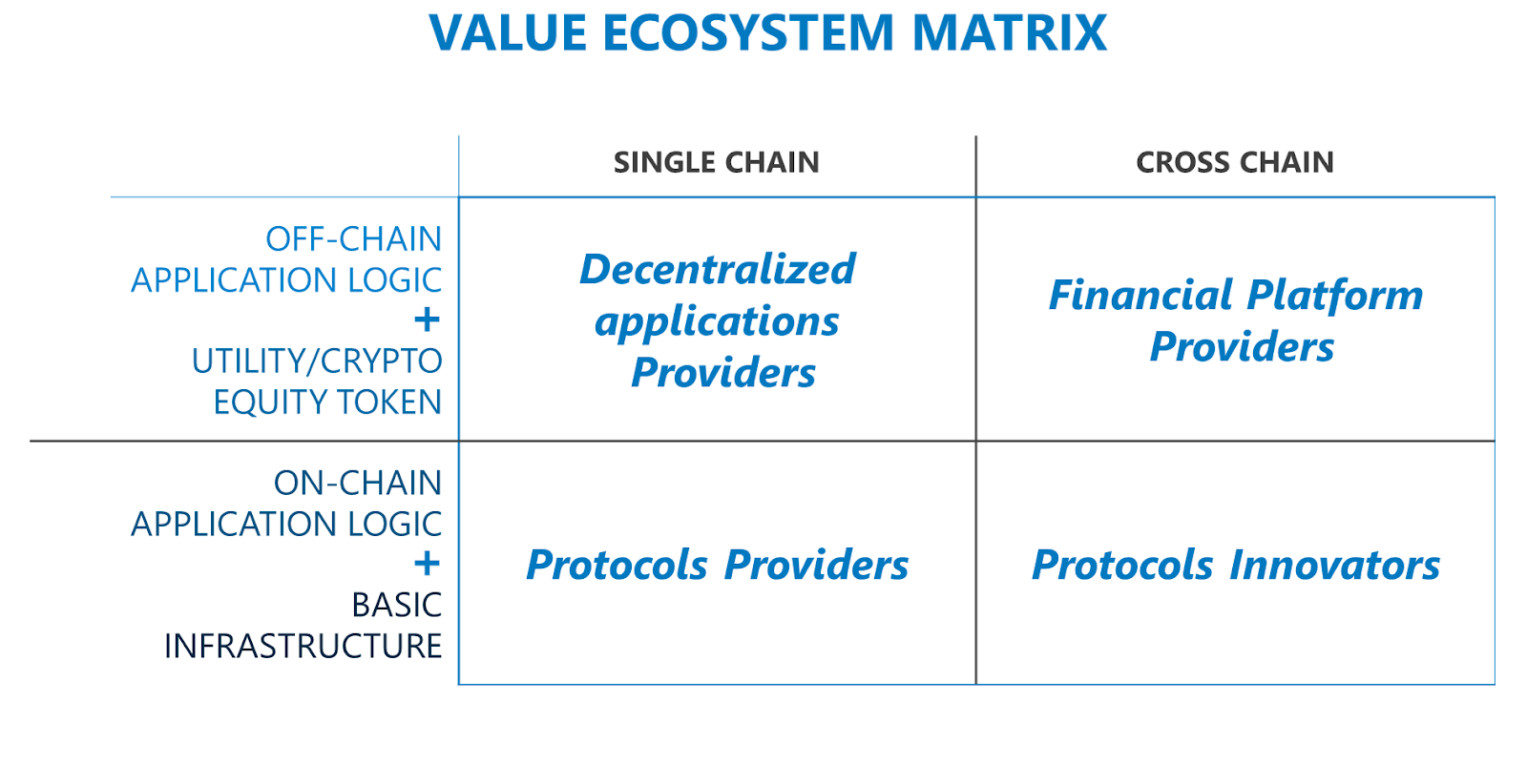

For the

classification of the key archetypal actors and their strategic positioning

with respect to the different blockchains available on the market, the

framework was complemented with an additional dimension considering whether the

company analysed was operating on a single blockchain or on multiple

blockchains. This resulted in a two by two ecosystem matrix answering RQ #1 and

identifying four strategic positions, one for each quadrant (Figure 3):

- Decentralized-application Providers

- Protocol Providers

- Financial Platform Providers

- Protocol Innovators.

Figure 3. Four strategic

positions

By placing the

ventures analysed in the different quadrants, it was subsequently possible to

cluster them into eleven archetypal actors (RQ #2): five of which positioned in

the distributed-applications providers quadrant and two situated in each of the

other quadrants (Figure 4). In this respect, it is important to note that while

DLTs are still in an “infrastructural phase”, that is to say a phase in which

enabling infrastructures are still being developed, a dominant design has not

emerged yet and most of the value generated is captured by the lower layers of

the technological stack [2]. Moreover, the upper left quadrant - where

distributed applications (DApp) are designed - represents a very fruitful

business model innovation sandbox for devising approaches that have the

potential to disrupt large rent-seeking incumbents across many different

industries in the long-term.

Figure 4. Eleven archetypal

actors

From the analysis

of the real life actors, it was subsequently possible to single out one or more

business models that could be associated to each archetypal actor. To

exemplify, among the mining companies analysed, four business models were

identified: (1) solo mining in which

the mining activity is conducted by a single company fully shouldering the

infrastructural costs and the risks associated with the mining activity; (2) pool mining in which companies are

sharing their infrastructure and the risk associated to mining; (3) cloud mining in which the company is

renting its computing infrastructure to third parties thus shifting the risk

associated with mining on the clients; and (4) mining marketplaces that are acting as brokers between

infrastructure owners and buyers of mining services.

Due to length

constraints, it is not possible to discuss in-depth all the business models

identified, nevertheless for each of them a Business Model Canvas explaining

the underlying value logic has been inserted in the appendix of the

presentation linked at the bottom of the post.

Figure 5. Twenty emerging business models

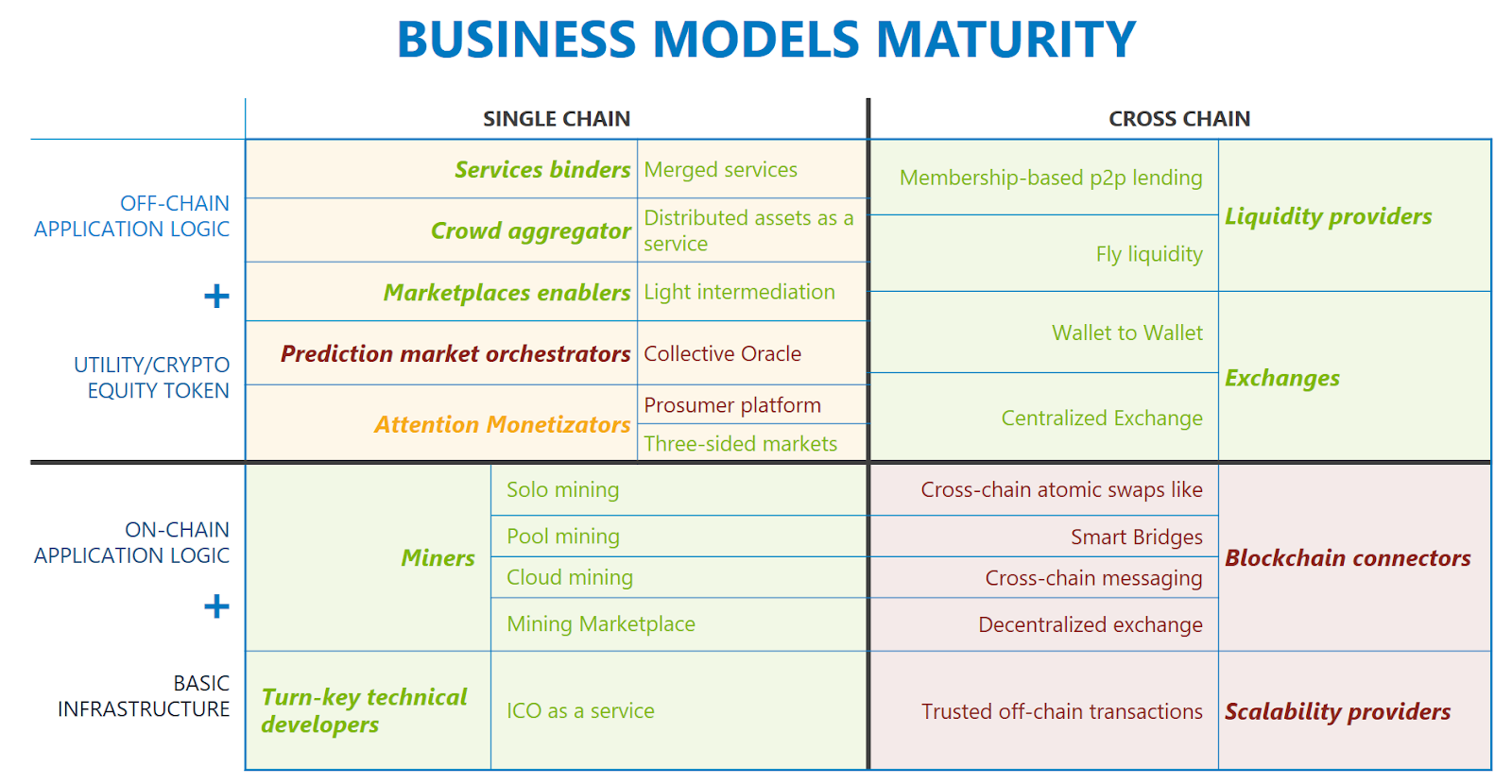

Finally, the

analysis of the thirty-two ventures brings to the fore dissimilar maturity

levels in terms of business model robustness for the various quadrants. More

specifically, the quadrants of protocol providers (lower-left) and that of

financial platform providers (upper-right) show a higher level of maturity in

terms of presence of a wide users’ base, identification of a clear value

proposition and tested value appropriation mechanisms. For what concerns the

other two quadrants instead, the situation is diversified among the actors

operating in the distributed applications quadrants (upper-left) while a low

level of maturity is present in the protocol innovators quadrant (lower-right)

which is made up of companies that are still exploring possible business models

for solving technical scalability issues.

Figure 6.

Business models maturity

To conclude this

post, we would like to share a number of reflections on the relationship

between blockchain and business strategy spurred by the analyses conducted

during the exploratory study.

First, a clear

understanding of the ingredients composing a full stack blockchain-based

solution needs to be acquired by CEOs willing to leverage blockchain in their

core business activity. In this respect, the blockchain value ecosystem

framework provides an accurate yet intuitive instrument for choosing the

appropriate level of vertical integration in the adoption and development of

blockchain-based solutions.

Second, four

strategic positions were identified with significant differences in terms of

capital intensity, technical proficiency required and depth of understanding of

the overall blockchain ecosystem. Choosing the right position for a venture

requires a careful analysis of the presence, possibility to access and ability

to manage the above aspects.

Third, twenty

business models were mapped with different levels of maturity with respects to

their ability to clearly identify their value proposition and the mechanisms

for capturing part of the value created. In this respect, the availability of

significant financial resources for startups at a very early stage of development combined with the presence of

seigniorage economic benefits coming from the possibility to mint tokens, in

many instances has reduced the pressure on cash flows thus allowing companies

to focus more on technical challenges. While this in the short-term this may

help raising the level of technological excellence of the blockchain ecosystem,

in the long-run it could pose serious sustainability challenges.

Finally, from a business model perspective, the emergence of blockchain technologies seems to

have generated three types of innovations: (1) the birth of business models for

blockchain-specific activities such as mining; (2) the possibility to combine

into a single business model activities previously conducted by different

players (eg: payments & reputation, chat & payments); (3) the emergence

of light intermediation opportunities in which the middleman may adopt

revenue-sharing mechanisms that promote a fairer redistributions of the overall

value generated by all the engaged stakeholders.

Should you be

interested in discussing more in depth the results of the study, don’t hesitate

to get hold of me via Linkedin or Twitter.

Research wants to be free, but it is costly to produce. Please consider supporting our market education activity by making a donation.

EOS account: cryptoenrico

BTC: https://tippin.me/@egferro

Enrico Ferro.

[1] Coindesk, 2018, “State of Blockchain Q1

2018” Retrievable at link

[2] Pantera

Capital, 2017, “VC’s Missing 97% of the Trade” Retrievable at link

Business Models for Blockchain-based Ventures from Enrico Ferro

Watch my interview with David Orban in which we talk about business models for blockchain.

good job

ReplyDeleteThanks for the appreciation Cyrus.

ReplyDeleteThanks for picking out the time to discuss this, I feel great about it and love studying more on this topic. It is extremely helpful for me. Thanks for such a valuable help again. blockchain jobs

ReplyDeleteThanks for providing information about blockchain training technology

ReplyDeleteYes, I am entirely agreed with this article, and I just want say that this article is very helpful and enlightening. I also have some precious piece of concerned info !!!!!!Thanks. bitcoin price

ReplyDeleteExcellent blog. Good content and very well explained. Thanks for sharing this blog. Blockchain Training In Bhubaneswar

ReplyDeleteCheck out this list of startups blockchain . Article to learn more about bitcoin.

ReplyDeleteEverything You Need To Know About The Cryptocurrency Wallet GlobalPay is wondering about the word Cryptocurrency With the growth in the cost and demand of this bitcoin, it generated excitement and excitement among all of the company investors as well as the organizations.

ReplyDeleteThe Invention of the blockchain technology and Bitcoin gave rise to the next generation of the blockchain micropayments network.

ReplyDeletei really like this article please keep it up. https://blockchainwhispers.com

ReplyDeleteIm grateful for the article post. Keep writing. Blockchain Whispers

ReplyDeleteNice article… very useful

ReplyDeletethanks for sharing the information.

servicenow training

Hiii...Thanks for sharing Great info...Nice post...Keep move on....

ReplyDeleteBlockchain Training in Hyderabad

ReplyDeleteNice info.Thanks for sharing this article Blockchain Online Training

Top Blockchain Online Training

Best Blockchain Online Training

azure online training provides all the azure services in detailed

ReplyDeleteTop rated, Leading finance assessment company in Eugene | Oregon

ReplyDeleteCSK Dynamic Ventures LLC in Eugene | Oregon

Contact CSK Dynamic Ventures LLC in Eugene | Oregon

Best Ventures for Corporate Growth in Eugene | Oregon

I got what you mean , thanks for posting .Woh I am happy to find this website through google. điều kiện du học Nhật Bản

ReplyDeleteIt is perfect time to make some plans for the future and it is time to be happy. I’ve read this post and if I could I desire to suggest you few interesting things or tips. Perhaps you could write next articles referring to this article. I want to read more things about it! huffexpress

ReplyDeleteThanks you for sharing this unique useful information content with us. Really awesome work.

ReplyDeleteConstruction Services Clapham

Leading cryptocurrency exchange software development company in USA

ReplyDeleteThere are many blockchain development companies but we are delivering best cryptocurrency exchange software all over the United states

Nice Post. I like your blog. Thanks for Sharing.

ReplyDeleteBlockchain Training Institute in Noida

Pretty article! I found some useful information in your blog, it was azure tutorial awesome to read, thanks for sharing this great content to my vision, keep sharing.

ReplyDeleteThe global gaming industry is evolving every day and providing gamers with games like real-life experiences using top-notch VR technology. In the future, we would see even more refined, crisp and clear real-world experiences with the advancements in VR. Get the best blockchain development services from the top blockchain development company which benefits like transparency, security, reduced costs, traceability and quick and highly efficient.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteThe Napoleon group has been creating overperforming methods for greater than 2 years on various crypto properties (Bitcoin, Ethereum, Litecoin, Ripple, Bitcoin Cash, Binance and also EOS). With these techniques, a financier has sufficient alternatives to start taking care of a portfolio and also constructing of measurable strategies. Auto crypto bot

ReplyDeleteWe have sell some products of different custom boxes.it is very useful and very low price please visits this site thanks and please share this post with your friends. Investment Opportunities

ReplyDeleteThanks for the blog loaded with so many information. Stopping by your blog helped me to get what I was looking for. Write for us business

ReplyDeleteIs business name avaiable Hey, i value your work and dedication. I was in fact just talking with a business owner the other day, and shared with him how to carry out what you are explaining in a comparable way for business naming. In your question, is business name available in US? Well, that question can be effortlessly answered with the tool i linke

ReplyDeleteHi everyone, I saw comments from people who had already got their loan from Anderson Loan Finance. Honestly I thought it was a scam and then I decided to make a request based on their recommendations because i was desperately in need of a loan. A few days ago, I confirmed in my personal bank account amounting to $ 12,000 , which I requested for business. This is really good news and I am so happy that I advise all those who need a real loan and who are sure to reimburse to apply through their email (Fax) +1 315-329-6320

ReplyDeleteThey are able to lend you a loan.

Contact Mr Anderson

E-mail: andersonraymondloanfinance@gmail.com

Telephone: +1 315-329-6320

Visit the office address @ (68 Fremont Ave Penrose CO, 81240) .

so happy to find good place to many here in the post, the writing is just great, thanks for the post. GRE代考

ReplyDeleteI am very enjoyed for this blog. Its an informative topic. It help me very much to solve some problems. Its opportunity are so fantastic and working style so speedy. bitcoin price prediction 2030

ReplyDeleteThey're produced by the very best degree developers who will be distinguished for your polo dress creating. You'll find polo Ron Lauren inside exclusive array which include particular classes for men, women. KIU

ReplyDeleteThey're produced by the very best degree developers who will be distinguished for your polo dress creating. You'll find polo Ron Lauren inside exclusive array which include particular classes for men, women. KIU

ReplyDeleteHello everyone, Are you into trading or just wish to give it a try, please becareful on the platform you choose to invest on and the manager you choose to manage your account because that’s where failure starts from be wise. After reading so much comment i had to give trading tips a try, I have to come to the conclusion that binary options pays massively but the masses has refused to show us the right way to earn That’s why I have to give trading tips the accolades because they have been so helpful to traders . For a free masterclass strategy kindly contact (paytondyian699@gmail.com) for a free masterclass strategy. He'll give you a free tutors on how you can earn and recover your losses in trading for free..

ReplyDeleteYou actually make it look so easy with your performance but I find this matter to be actually something which I think I would never comprehend. It seems too complicated and extremely broad for me. I'm looking forward for your next post, I’ll try to get the hang of it! Buy Antminer K5

ReplyDeleteI think more information should be provided in the blog!!

ReplyDeleteIt has fully emerged to crown Singapore's southern shores and undoubtedly placed her on the global map of residential landmarks. I still scored the more points than I ever have in a season for GS. I think you would be hard pressed to find somebody with the same consistency I have had over the years so I am happy with that. Fotografin

ReplyDeleteYou might comment on the order system of the blog. You should chat it's splendid. Your blog audit would swell up your visitors. I was very pleased to find this site.I wanted to thank you for this great read!! Fotografin

ReplyDeleteI found that site very usefull and this survey is very cirious, I ' ve never seen a blog that demand a survey for this actions, very curious...

ReplyDeleteбиткоин на приват

A good blog always comes-up with new and exciting information and while reading I have feel that this blog is really have all those quality that qualify a blog to be a one sports authority

ReplyDeleteI’m happy I located this blog! From time to time, students want to cognitive the keys of productive literary essays composing. Your first-class knowledge about this good post can become a proper basis for such people. nice one Timeshare Freedom Group

ReplyDeleteYou make so many great points here that I read your article a couple of times. Your views are in accordance with my own for the most part. This is great content for your readers. Capital Funding

ReplyDeleteExcellent Blog! I would like to thank for the efforts you have made in writing this post. I am hoping the same best work from you in the future as well. I wanted to thank you for this websites! Thanks for sharing. Great websites! small business directory

ReplyDeletegreat page

ReplyDeletePHP Training in Chennai | Certification | Online Training Course | Machine Learning Training in Chennai | Certification | Online Training Course | iOT Training in Chennai | Certification | Online Training Course | Blockchain Training in Chennai | Certification | Online Training Course | Open Stack Training in Chennai |

Certification | Online Training Course

I wanted to thank you for this great read!! I definitely enjoying every little bit of it I have you bookmarked to check out new stuff you post. B2B Email List

ReplyDeletehttps://onlineitguru.com/blockchain-course.html

ReplyDeletehttps://onlineitguru.com/blockchain-course.html

article is very interesting and effective. Thank you and good luck for the upcoming articles Learn blockchain online training

blockchain online course

You completely match our expectation and the variety of our information. Oregon Business Registry

ReplyDeleteI curious more interest in some of them hope you will give more information on this topics in your next articles. Get admission in Canada

ReplyDeleteMoney Gadget

ReplyDeleteMoney Gadget

Money Gadget

Money Gadget

Money Gadget

Money Gadget

Money Gadget

Money Gadget

Your blog has piqued a lot of real interest. I can see why since you have done such a good job of making it interesting. I appreciate your efforts very much. internal audit tracking software

ReplyDeleteWow!! Really a nice Article about Angular Js. Thank you so much for your efforts. Definitely, it will be helpful for others. I would like to follow your blog. Share more like this. Thanks Again.

ReplyDeletepython training in bangalore

python training in hyderabad

python online training

python training

python flask training

python flask online training

python training in coimbatore

Thanks for one marvelous posting! I enjoyed reading it; you are a great author. I will make sure to bookmark your blog and may come back someday. I want to encourage that you continue your great posts.

ReplyDeleteFull Stack Training in Chennai

Full Stack Course Chennai

Full Stack Training in Bangalore

Full Stack Course in Bangalore

Full Stack Training in Hyderabad

Full Stack Course in Hyderabad

Full Stack Training

Full Stack Course

Full Stack Online Training

Full Stack Online Course

This is my first visit to your web journal! We are a group of volunteers and new activities in the same specialty. Website gave us helpful data to work. cfa books pdf

ReplyDeleteOnce you promote your home business a while and start getting sales, determine what you'll need to do to create a steady cash system for the future. alcohol free hand sanitser

ReplyDeleteA great website with interesting and unique material what else would you need. b2bguruclass

ReplyDeleteThey're produced by the very best degree developers who will be distinguished for your polo dress creating. You'll find polo Ron Lauren inside exclusive array which include particular classes for men, women. More

ReplyDeleteyou have got outdone yourself this develop outdated. It is probably the great, maximum immediate grade by grade manual that i have ever seen. https://www.blaze.me/dispensary-pos-software/

ReplyDeleteThis is a wonderful article, Given so much info in it, These type of articles keeps the users interest in the website, and keep on sharing more ... good luck. custom challenge coins

ReplyDeleteI read that Post and got it fine and informative. Please share more like that... custom challenge coins

ReplyDeleteThanks for this great post, i find it very interesting and very well thought out and put together. I look forward to reading your work in the future.Top cryptocurrency blog

ReplyDeleteThis post is perfect for getting ideas about Business Models for Blockchain-based Venture. Businessmen should get lesson from this valuable information. Essay Writing Services

ReplyDeletei am always looking for some free stuffs over the internet. there are also some companies which gives free samples. Learn Microsoft Dynamics 365 Business Central

ReplyDeleteThis is such a great resource that you are providing and you give it away for free. I love seeing blog that understand the value of providing a quality resource for free. cfa level 1 study material

ReplyDeletehello!! Very interesting discussion glad that I came across such informative post. Keep up the good work friend. Glad to be part of your net community. VoIP service providers in India

ReplyDeleteforex if you have confined or no information about forex at all. forex exchange

ReplyDeleteHere you will learn what is important, it gives you a link to an interesting web page: best blockchain investment firm

ReplyDeleteWow, cool post. I'd like to write like this too - taking time and real hard work to make a great article... but I put things off too much and never seem to get started. Thanks though. commercial electrical contractors

ReplyDeleteI am genuinely thankful to the holder of this web page who has shared this wonderful paragraph at at this place Click

ReplyDeleteThanks for the lucid content. Your knowledge on the subject and dedication is overtly visible.

ReplyDeleteThanks!

https://www.login4ites.com/

Thanks for the informative and helpful post, obviously in your blog everything is good.. 토토사이트

ReplyDeleteThat is really nice to hear. thank you for the update and good luck. local website solutions

ReplyDeleteI found that site very usefull and this survey is very cirious, I ' ve never seen a blog that demand a survey for this actions, very curious... Graphic Design Company

ReplyDeleteI think that thanks for the valuabe information and insights you have so provided here. Best Domain Name Registration Australia

ReplyDeleteThis blog is really great. The information here will surely be of some help to me. Thanks!. mastering physics

ReplyDeleteAwesome blog. I enjoyed reading your articles. This is truly a great read for me. I have bookmarked it and I am looking forward to reading new articles. Keep up the good work! sulopay

ReplyDeleteYou completely match our expectation and the variety of our information. 스포츠티비

ReplyDeleteVery nice article, I enjoyed reading your post, very nice share, I want to twit this to my followers. Thanks!. 123 movie

ReplyDeleteThank you very much for this useful article. I like it. online jobs 2021

ReplyDeleteIt is a completely interesting blog publish.I often visit your posts for my project's help about Diwali Bumper Lottery and your super writing capabilities genuinely go away me taken aback.Thank you a lot for this publish 안전놀이터

ReplyDeleteI have added and shared your site to my social media accounts to send people back to your site because I am sure they will find it extremely helpful too. 파워볼사이트

ReplyDeleteThis is actually the kind of information I have been trying to find. Thank you for writing this information. 먹튀검증커뮤니티

ReplyDeleteI'm constantly searching on the internet for posts that will help me. Too much is clearly to learn about this. I believe you created good quality items in Functions also. 먹튀검증업체

ReplyDeleteHmm… I interpret blogs on a analogous issue, however i never visited your blog. I added it to populars also i’ll be your faithful primer 메이저놀이터

ReplyDeleteThis article was written by a real thinking writer.I agree many of the with the solid points made by the writer 먹튀검증

ReplyDeleteThis is the reason it really is greater you could important examination before creating. It will be possible to create better write-up like this. 먹튀폴리스꽁머니

ReplyDeleteVery useful post. This is my first time i visit here. I found so many interesting stuff in your blog especially its discussion. Really its great article. Keep it up 안전놀이터

ReplyDeleteI just found this blog and have high hopes for it to continue. 안전놀이터

ReplyDeleteI have read your article, it is very informative and helpful for me. I admire the valuable information you offer in your articles. Thanks for posting it 먹튀검증

ReplyDeleteYes, I am entirely agreed with this article, and I just want say that this article is very helpful and enlightening. I also have some precious piece of concerned info !!!!!!Thanks. 토토사이트

ReplyDeleteIt's always exciting to read articles from other writers and practice something from their web sites 먹튀검증

ReplyDeleteHey There. I found your blog using msn. This is a very well written article. I’ll be sure to bookmark it and come back to read more of your useful info. Thanks for the post. I’ll definitely return. small business marketing firms

ReplyDeleteExtremely pleasant and fascinating post. I was searching for this sort of data and appreciated perusing this one. Continue posting. Much obliged for sharing. EBWaite

ReplyDeleteExtremely pleasant and fascinating post. I was searching for this sort of data and appreciated perusing this one. Continue posting. Much obliged for sharing. courtier immobilier Engel & Völkers

ReplyDeleteExtremely pleasant and fascinating post. I was searching for this sort of data and appreciated perusing this one. Continue posting. Much obliged for sharing. patio furniture chairs

ReplyDeleteExtremely pleasant and fascinating post. I was searching for this sort of data and appreciated perusing this one. Continue posting. Much obliged for sharing. Courtier immobilier gatineau

ReplyDelete"It’s going to be ending of mine day, but before finish I

ReplyDeleteam reading this fantastic article to improve my knowledge." yoga gatineau

"It’s going to be ending of mine day, but before finish I

ReplyDeleteam reading this fantastic article to improve my knowledge." courtier immobilier West Carleton

"Appreciation to my father who shared with me concerning this web site, this weblog is genuinely remarkable.

ReplyDelete" real estate broker West Carleton

This is very nice one and gives indepth information. Thanks for this nice article. 이기자벳

ReplyDeleteFashion is exciting, so why should buying fashion items involve boring tasks walking around in one store after another?its time to boring more zing to fashion purchases

ReplyDeleteFashion App Development Company

Article is amazing. Thanks for sharing. eCommerce Development Company

ReplyDeleteHello There. I found your blog using msn. This is a very well written article. I’ll be sure to bookmark it and come back to read more of your useful info. 스웨디시

ReplyDeletePretty good post. I have really enjoyed reading your blog posts.Any way Here I am Specialist in Manufacturing of Movies, Gaming, Casual, Faux Leather Jackets, Coats And Vests See Clint Eastwood Poncho

ReplyDeleteYou have performed a great job on this article. It’s very precise and highly qualitative. You have even managed to make it readable and easy to read. You have some real writing talent. Thank you so much. convert pdf to jpg

ReplyDeleteTechBizLand is a blogging site that provides the latest information with respect to eCommerce, trending technologies, gadgtes and many more!

ReplyDeleteWow, great blog article I look forward to your kind cooperation.토토존보증업체

ReplyDeleteIt's great to have a place like this.Guess I will just bookmark this site.놀이터추천

ReplyDeleteI want to start a blog to write about everything that happens at school and

ReplyDeletewith friends…anonymously…any sugestions?.울산오피

Startup recruitment agency Really I enjoy your site with effective and useful information. It is included very nice post with a lot of our resources.thanks for share. i enjoy this post.

ReplyDelete

ReplyDeleteNice Post!

music streaming app development

fintech app development

This was really a very informative post and I am glad to offer a similar information by which you can create more Animated explainer videos

ReplyDeleteAn animated explainer video company grasp your business ideas and translate them into animated explainer videos or live videos crafted with thoughtful messaging. A creative design team, 2D animation company can come up with the proper sort of video as per our client’s approach. Be it for a product, a replacement venture you’re foraying into or anything that’s tough to elucidate to your audience , our team is adept at creating an animated video for business in multiple languages to support their vernacular requirements.

Thanks for sharing insight full thoughts I really enjoyed this post.

ReplyDeleteAnnotation Tool

Good info. Lucky me I discovered your blog by accident

ReplyDelete(stumbleupon).

I’ve book marked it for later!

I want to say thanks to you. I have bookmark your site for future updates. 網上交友平台

ReplyDeleteYou make so many great points here that I read your article a couple of times. Your views are in accordance with my own for the most part. This is great content for your readers. study health sciences in university of New Brunswick Canada

ReplyDeleteIf you are you ready to instill the advantages of Blockchain development in your business to get rid of all those problems that are holding back your productivity? For this purpose, you need to hire an experienced Blockchain development agency. That’s where we come in. Here at IIInigence, we stand proud as the best Blockchain development company in the USA . IIInigence LLC offer our clients top-notch Blockchain development services to secure their business space on top of increasing productivity and reducing cost.

ReplyDeleteI want to say thanks to you. I have bookmark your site for future updates compress pdf online

ReplyDelete

ReplyDeleteBEP20 token has been created on Binance’s own platform and it delivers some innovative features very easily. This token helps you make the most of blockchain technology and gives you the ability to take things to another level. Also, it enables you to address the issues of token users and resolved them with impeccable efficacy.

Develop Your Own Token Like BEP20 On Binance Smart Chain

For any query drop a mail at info@technoloader.com and ping on 91 7014607737

Amazing that you share this informative blog, Really looking forward to read artical like this.

ReplyDeletehitachi 1.5 ton 3 star split inverter ac

Very nice and informative blog.

ReplyDeleteGreat Post!

ReplyDeleteThanks for sharing!

News & magazine app development

Nice post check my site for super fast Satta king Result also check Sattaking

ReplyDeletei am always looking for some free stuffs over the internet. there are also some companies which gives free samples. 먹튀사이트

ReplyDeleteWonderful blog! I found it while surfing around on Yahoo News. Do you have any suggestions on how to get listed in Yahoo News? I’ve been trying for a while but I never seem to get there! Appreciate it. esa letter

ReplyDeleteI exactly got what you mean, thanks for posting. And, I am too much happy to find this website on the world of Google. 스포츠토토

ReplyDeleteImpressive web site, Distinguished feedback that I can tackle. Im moving forward and may apply to my current job as a pet sitter, which is very enjoyable, but I need to additional expand. Regards. 메이저사이트

ReplyDeleteHello I am so delighted I located your blog, I really located you by mistake, while I was watching on google for something else, Anyways I am here now and could just like to say thank for a tremendous post and a all round entertaining website. Please do keep up the great work. Buy Antineoplastic Drugs Online

ReplyDeleteNice post! This is a very nice blog that I will definitively come back to more times this year! Thanks for informative post. get muzz

ReplyDeleteGreat post, you have pointed out some fantastic points , I likewise think this s a very wonderful website. 먹튀검증

ReplyDeleteGreat Blog Post!!! Thanks for Sharing

ReplyDeleteOnline Wig Store

It is very interesting to see what positive impact blockchain technology will have on us.토토사이트

ReplyDeleteHello, I am a sports blog active in Korea.

ReplyDeleteThis is N토토

It is an honor to visit your site. If you have a chance, would you like to visit our site as well? I'll leave your address.

사설토토-사설토토사이트

사설토토 선택의 절대적으로 기준이 되는것은

장기간 안정적으로 먹튀없이 운영되어진곳이

첫번째가 되겠습니다.

일반사람이 구분하는것에는 한계가 있어서

토토사이트 검증 사이트를 통하여 알아보는것또한

토토사이트 검증 <---Click to go to my website

I apologize again if what I wrote was inconvenient,

and have a nice day.

This is Great Article. You are post informatics blog so keep posting.

ReplyDeleteHome Services App

Best Seo Service Company

Best Affordable Seo Services Delhi NCR

Top 10 CSBE Schools in Meerut

Desawer King Chart

Website Design Company Meerut

Satta King Live Online

Entertainment News Update

HOme Service providers’ app

Screensavers for Windows 10

Home Services App in India

I have been checking out a few of your stories and i can state pretty good stuff. I will definitely bookmark your blog tikpay

ReplyDelete

ReplyDeleteNice post. I used to be checking constantly this blog and I am impressed! Extremely useful info particularly the ultimate section 🙂 I take care of such information a lot. I was seeking this certain information for a long time. Thank you and best of luck.

Communication skills essay

Nice post! This is a very nice blog that I will definitively come back to more times this year! Thanks for informative post. Write for us business

ReplyDeleteGreat Blog post! thanks for sharing

ReplyDeleteBest Window Tint Film.

Varicose veins may develop secondary to deep vein thrombosis or regurgitation of a penetrating vein. 메이저사이트

ReplyDeleteWhen some one searches for his vital thing, thus he/she desires to be available

ReplyDeletethat in detail, so that thing is maintained over here.

풀싸롱

click me ( L-G )

This is a great inspiring article.I am pretty much pleased with your good work.You put really very helpful information. Keep it up. Keep blogging. Looking to reading your next post.

ReplyDeleteIndian Freeway Jacket

Thanks for taking the time to discuss this, I feel strongly that love and read more on this topic. If possible, such as gain knowledge, would you mind updating your blog with additional information? It is very useful for me. 토토사이트

ReplyDeleteThanks for providing recent updates regarding the concern, I look forward to read more. 대전마사지

ReplyDeletevery nice post, i surely really like this website, go on it 에볼루션카지노

ReplyDeleteI really enjoyed reading your article. I found this as an informative and interesting post, so i think it is very useful and knowledgeable. I would like to thank you for the effort you made in writing this article. Drive Scorpion Jacket

ReplyDeleteThis is such a great resource that you are providing and you give it away for free. I love seeing blog that understand the value of providing a quality resource for free. overseas education consultants

ReplyDeleteYou made such an interesting piece to read, giving every subject enlightenment for us to gain knowledge. Thanks for sharing the such information with us to read this... usa verified paypal account

ReplyDeleteWhat a superb content! You are indeed a prolific writer, the topic is well elucidated. I hope to see more of such post on my next visit. Great post! Goldcoders hyip template

ReplyDeleteReally I like your article it is easy to reading. You are a good blogger pls keep it up. Thank you so much. We offer incomparable Best Dissertation Writing Services

ReplyDeleteI was recommended this web site by my cousin. I am not sure whether this post is written by him as nobody else know such detailed about my trouble. You are incredible! Thanks! Hello very nice website!! Guy .. Beautiful ..Wonderful .. I’ll bookmark your web site and take the feeds additionally? I am glad to seek out so many helpful information here in the put up, we need develop more strategies in this regard, thanks for sharing. Excellent information on your blog, thank you for taking the time to share with us. Amazing insight you have on this, it’s nice to find a website that details so much information about different artists. 먹튀검증

ReplyDeletewhats up! I ought to have sworn i’ve visited this internet site earlier than but after browsing thru among the articles i found out it’s new to me. Although, i’m truly happy i discovered it and i’ll be book-marking it and checking again regularly! Thanks for each other informative site. The area else can also simply i get that sort of information written in such a perfect way? I've a venture that i’m simply now working on, and i have been on the look out for such records. I respect this newsletter for the nicely-researched content and awesome wording. I got so involved in this material that i couldn’t forestall reading. I'm impressed together with your work and skill. Thank you so much . Wow, amazing, i used to be wondering a way to therapy acne certainly. 먹튀검증

ReplyDeleteWhat else may additionally i get that type of info written in this type of best method? I've an undertaking that i'm simply now operating on, and i've been searching for such info. You completed some best points there. I did a seek at the subject and observed almost all humans will go with along with your blog. This is an superb motivating article. I am practically satisfied with your remarkable work. You put truely extraordinarily supportive information. Keep it up. Preserve blogging. Hoping to perusing your subsequent put up 카디즈에이전시

ReplyDeleteThanks for sharing detailed information

ReplyDeleteSan Diego Web Design Company .

it was a wonderful chance to visit this kind of site and I am happy to know. thank you so much for giving us a chance to have this opportunity..

ReplyDeletetag protocol cryptocurrency

This article was written by a real thinking writer. I agree many of the with the solid points made by the writer. I’ll be back. business management books pdf

ReplyDeleteThe post is written in very a good manner and it contains many useful information for me. prince group cambodia

ReplyDeleteGreat Blog

ReplyDeleteblockchain development company

This blog is very helpful information thank you so much for sharing this. Learn more about blockchain development for ethereum.

ReplyDeleteHey, I am happy to visit here thanks for the nice information. Kindly visit my site. sexual desires

ReplyDeleteYou can find your own powerful CPU and GPU products and their campaigns. Antminer L7 9500mh 9160mh for Dogecoin Litecoin BITMAIN Miner Machine. Live customer service and sopports . Many many shippings options. 100% Guaranteed products. And Also International shipping. "s19 antminer

ReplyDeletes19 95th price

goldshell kd2

s19 miner

the windrift

antminer for sale

avalon suites

bitmain antminer l7

s19j pro

bitmain antminer z15"

I like to look at an article that makes individuals think.

ReplyDeleteLikewise, thank you for allowing me to remark! "

토토사이트

Amazing write-up!!!

ReplyDeleteDEFI SMART CONTRACT

The blog is very interesting. This is one of the best blogs on commenting. Carry on writing such useful stuff. Keep it up!! Thanks for sharing…

ReplyDeleteDEFI SMART CONTRACT

A ready to established fuel on-demand application service for a faster time to market, without a significant time or money.

ReplyDeletehttps://lilacinfotech.com/what-we-do/fuel-on-demand-app-development-india

useful Information

ReplyDeletenft-marketplace-become-popular

Opensea clone script

ReplyDeleteAxie infinity clone script

Rarible clone script

Zed run clone script

Cryptopunks clone script

responsive website design concept is spreading rapidly and becoming the norm. Main benefit of responsive web design is flexible to adapt different screens of website or mobile devices.

ReplyDeleteVery nice article, I like it very much.

ReplyDeleteI wrote a review myself. If you want to read, here is the link: https://bit.ly/32RHAvy and https://bit.ly/3LtFCTY

Its a very good discussion about business models for blockchain , you have explained nicely.

ReplyDeleteInovies

ReplyDeleteVERY INFORMATIVE AND KNOWLEDGEABLE ARTICLE…..THANKS FOR SHARING……

TOKEN DEVELOPMENT COMPANY

Thank you for your post, I look for such an useful and beautiful article for a long time, today I found it finally. this post gives me lots of advice it is very useful for me.

ReplyDeleteSerumswap Clone Development

ReplyDeleteThank you for sharing information, and I am a morce decoder as well. In simple terms, this article is very interesting, and I'd like to share my most recent article with you. Please visit my blog post based on morse code

This article is awesome. I was looking for similar information. Thanks for sharing this with us. I would like to share this article with you which is about a Space bar counter.This Spacebar Test has multiple time frame interpretations so that people can use and conduct

ReplyDeletespace bar speed tests Read and find out more!

Great Blog Post!!! Thanks for Sharing

ReplyDeletePeptides for sale online .

The article was enjoyable to read. This is extremely useful and valuable information. Thank you kindly. Please see my previous post Keyboard not working . This post explains some of their techniques in detail, and you should be able to test your keyboard by visiting the article. Please read on to find out more.

ReplyDeletesmm panel

ReplyDeleteSMM PANEL

İS İLANLARİ BLOG

İNSTAGRAM TAKİPÇİ SATIN AL

HİRDAVATCİ BURADA

beyazesyateknikservisi.com.tr

Servis

TİKTOK JETON HİLESİ

beykoz lg klima servisi

ReplyDeleteçekmeköy samsung klima servisi

ataşehir samsung klima servisi

maltepe arçelik klima servisi

kadıköy arçelik klima servisi

kartal samsung klima servisi

ümraniye samsung klima servisi

ümraniye mitsubishi klima servisi

tuzla toshiba klima servisi

Thank you for sharing. If you are looking for a company to help you build blockchain service, you can visit us through:

ReplyDeleteAgile Tech Vietnam

Microsoft Azure Training In Chennai - Login360

ReplyDeleteA premierMicrosoft Azure Training course Chennai

in Chennai is Login360. We provide a variety of software-related courses with complete placement assistance.

Our instructors and subject-matter specialists have been offering our students top-notch IT training in a wide variety of popular azure courses.

Our courses are frequently updated, cover the most popular and up-to-date areas in IT, and we offer top-notch training in azure technologies.

We provide placement help for recent grads (recent graduates). provide advice to all qualified applicants.

Contact Details:

Name: Login360 Software Training Institute

Address: No-06, Ground Floor, 5th Main Road, Vijaya Nagar Velachery, Chennai – 600042.

Phone: 6385872810

Website: https://login360.in/microsoft-azure-training-courses-chennai/

wordpress website design studio Need professional WordPress Web Design Services? We're experts in developing attractive mobile-friendly WordPress websites for businesses. Contact us today!

ReplyDeleteI once lost an incredible amount of money to a fake Binary option Brokers i think about 3years ago, It all started from a phone call and after some persuasion I decided to invest, after months of constant investment about 130k$, I decided to ask for a payout this was the beginning of my turmoil, to my dismay I was still asked to invest more. Being a Single mother this really affected me and despite all efforts to contact them failed. I was introduced to the ( wizesafetyrecovery @ GMAIL COM ); he took legal actions against them and he helped me retrieve my funds. I couldn’t be more thankful

ReplyDeleteNice blog. Thank-you, for sharing such great information.cryptocurrency exchange software development company

ReplyDeleteBest blog I have ever read!!

ReplyDeleteSchool in Varanasi

Nice and amazing post. I really appreciate you on good effort. Thanks a lot for share great Blog. i like your work. we also provide . for more information visit on our website.best blockchain explorer

ReplyDeletethanks for sharing the informational blog. bep20 token development

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteGreat thoughts on blockchain in financial industry! It effectively highlights how fintech app development service providers are leveraging blockchain technology in their apps to enhance security and transparency. I'm excited to see how this will revolutionize the fintech industry.

ReplyDeleteHire Blockchain Developer that can help you explore the potential benefits of blockchain solutions for your business. Whether you are looking to improve supply chain efficiency, enhance transparency and security in your transactions, or create new revenue streams through blockchain-based products or services, we can provide you with the guidance and expertise you need to make informed decisions about how to leverage blockchain services to achieve your business goals.

ReplyDeleteEmpower your venture with iMeta Technologies Axie Infinity Clone Script , enabling the creation of digital pet NFT games. Our script allows you to build a distinctive NFT Gaming Platform similar to Axie Infinity, providing a seamless and customizable gaming experience. Explore the possibilities of blockchain gaming with our innovative solution. Request a free demo of our Axie Infinity Clone Script. It encompasses features like battles, breeding, land, and a marketplace, along with a scholarship and ranking system.

ReplyDeleteRight way law recovery services are the recommended company that guides swiftly in every steps needed in getting back trackable transactions from brokers. As a consumer in financial disputes, while taking such steps try documenting everything that was communicated that leads to transactions, and steps you took to address the situation. This documentation will be helpful for records, submitting all relevant documents increases A1 quality to affected account before clarifying and the processing of the maxed amount stolen into affected wallet address. Question for help via Email;

ReplyDeleterightwaylawrecoveryservice@gmail.com.

Telegram +1 513 602 3179

WhatsApp +1(336)3942139

Great post. Thanks for sharing.

ReplyDeleteMeme Crypto Coin Development

My name is Frank S. Monnett, and I want to share my incredible experience with Santoshi Hackers Intelligence (SHI). On June 1, 2023, I faced a devastating loss of $65,600 through my Coinbase account. When the SHI team explained how they would use Tokenomics to recover my funds, I was initially skeptical, thinking it might just be another marketing gimmick.

ReplyDeleteTo my absolute shock, within less than 24 hours, I saw my $65,600 successfully restored to my Coinbase Ethereum wallet. SHI’s expertise in cybersecurity and their deep understanding of the crypto ecosystem are nothing short of remarkable.

SHI plays no games—they are professionals who deliver on their promises. I cannot thank the team enough for their swift and effective action on my case. I wholeheartedly recommend Santoshi Hackers Intelligence to anyone facing similar issues. Their work is truly extraordinary! [ santoshihacker@hotmail.com }

Live streaming on blockchain ensures security, transparency, and decentralized content distribution for creators and viewers. PerfectionGeeks Technologies offers cutting-edge blockchain streaming solutions.

ReplyDeleteVery useful information! The IT industry is evolving rapidly, and blockchain is truly disrupting the digital era. Businesses that adapt early will have a huge advantage. If you're looking to explore Web3 or build secure decentralized solutions, now’s the time to hire a blockchain developer. At CodeHazel, we offer professional blockchain development services tailored to your business needs. Let’s build the future together!

ReplyDeleteThis post deserves a round of applause—truly top-notch content!

ReplyDeleteAttorney to Review Employment Contract!

I JUST RECOVERED MY SCAMMED BITCOIN. It’s the first time since 4 months I contacted honest people through internet, I lost money with scam crypto company, I contacted 3 recovery companies, it turned all of them are scammers, Until I contacted: zattechrecovery At G mail Dot Com, I sent them all information’s about the scam company and After giving them the information they needed from me, It took them only 24 to refund my 150,000 USD back to me. I wrote this review, to thank this company for their honesty and those out there in need of help.

ReplyDeleteGreat breakdown of blockchain business models! As an NFT marketplace development company, we often lean on frameworks like yours to map out the right layer of integration—whether it’s smart‑contract basics or full multi‑chain solutions. Understanding where we sit in the ecosystem helps us build platforms that balance user experience, security, and growth. Thanks for sharing these clear insights!

ReplyDeleteCool

ReplyDeleteIt takes more than just reciting incantations and brandishing a magic wand to retrieve lost Bitcoins. It takes perseverance, technical know-how, and comprehension of blockchain technology to make sure that your lost Bitcoins are returned back to you. For that to happen, you need to get a professional instead of settling for mediocre. There are many advantages of selecting Intel Fox Recovery Services for your bitcoin retrieval needs. These team of geniuses are there for you at every step, offering professional advice and effective solutions. Your peace of mind is their top priority at Intel Fox Recovery so just be rest assured that your security and confidentiality are paramount throughout the recovery process. With stringent measures in place to safeguard your sensitive information, you can trust the team to handle your case with the utmost discretion and care. A successful bitcoin recovery emphasizes on how crucial it is to have a reliable partner when overcoming the challenges of recovering digital assets. Intel Fox Recovery stands out as a ray of light for anyone looking to recover their stolen bitcoins because of their dedication to quality, security, and secrecy. Binary options, in my opinion, are more of a gamble than an investment especially if your broker chooses to make the investment on your behalf. It hurts to invest and lose, thanks to my broker, who invested on my behalf and lost $110,000 USD. I was able to lose all of my money because I trusted a broker I came in contact with online. If you have fallen into this situation, you need to know that time is critical when it comes to retrieving misplaced bitcoins. The likelihood of a successful retrieval might be considerably decreased by postponing recovery attempts and the consequences can be messy. Address your issues with Intel Fox Recovery Services in time and preferably send them an email: intelfoxrecovery [@] mail[.]com

ReplyDeleteThis program truly supports working-class families. CCS estimator

ReplyDeleteThanks for creating such a clear and structured post, it helped me understand well. Read this article to learn more Coreball. Coreball Unblocked helps players enhance timing and reaction skills through continuous play.

ReplyDelete